Online gambling continues to gobble up an ever-larger share of the overall UK market, while gaming machines in betting shops saw their share decline for the first time ever.

Online gambling continues to gobble up an ever-larger share of the overall UK market, while gaming machines in betting shops saw their share decline for the first time ever.

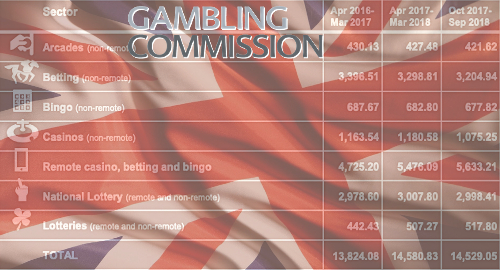

On Thursday, the UK Gambling Commission (UKGC) released its latest statistics on the UK market for the 12 months ending September 2018. During that span, UK-licensed operators generated gross gambling yield (GGY) of £14.5b, which the UKGC says represents a 0.4% decline from the 12 months ending March 2018 (although they originally reported GGY of £14.4b during that period, so bear in mind that these figures apparently aren’t carved in stone).

Regardless, online gambling’s growth continued unabated, accounting for GGY of £5.63b and a market share of 38.8%, up from 37.1% in the previous period. Online casino games accounted for nearly £3b (+1.8%) of this total, two-thirds of which came via slots. While online race and sports betting was essentially flat at £2.1b, overall online ‘betting’ was up 3.7% thanks to exchange betting rising 21% to nearly £343m and bingo improving 7.6% to £177.6m.

Land-based bookmakers’ GGY ranked second in the pecking order with £3.2b, down around £94m from the previous period. Gaming machines continued to account for the bulk (59.2%) of bookmakers’ GGY but this number fell £5.6m to £1.83b. It’s a modest decline but it’s the first backward step the machine category has taken since the UKGC began keeping score.

It’s worth noting that this decline came prior to the UK government’s forced reduction in maximum betting stakes on fixed-odds betting terminals (FOBT), which took effect on April 1. The number of FOBTs in operation at the end of the reporting period was 33,190, over 500 fewer than were in operation during the previous period and the lowest number of active FOBT in seven years.

The number of betting shops was also at a new low of 8,423, down from 8,555 in the previous period and well off the market-high of 9,128 at the end of March 2012. Ladbrokes and Gala Coral accounted for the overwhelming bulk of these closures as their parent firm GVC Holdings looked for the dreaded ‘efficiencies’ on its balance sheet.

As for the other gambling verticals, National Lottery sales and GGY were both essentially flat at £6.9b and £3b, respectively. Land-based casino GGY was down 11.4% to £859m, largely due to punto banco (baccarat) GGY tumbling by two-fifths to £138.8m. Land-based bingo GGY was down 1% to £355.3m. Remote virtual betting, which had been on a noticeable upswing, slipped 4.2% to £81.8m.

The UKGC has been cracking the whip regarding online operators’ social responsibility obligations, and self-exclusions shot up nearly 11% to over 1.5m during the period, while known breaches of these exclusions were up 13% to 99k. Operators challenged over 100k gamblers (after they’d gambled, mind you) regarding their age, up 28% from the previous period.