Strong progress with H1 revenue growth of 37%, Adjusted EBITDA growth of 56% and strong current trading resulting in the Board now anticipating that FY20 Adjusted EBITDA will be significantly ahead of its prior expectations

Strong progress with H1 revenue growth of 37%, Adjusted EBITDA growth of 56% and strong current trading resulting in the Board now anticipating that FY20 Adjusted EBITDA will be significantly ahead of its prior expectations

888, one of the world’s most popular online gaming entertainment and solutions providers, announces its half-yearly results for the six months ended 30 June 2020 (the “period”).

Financial Highlights

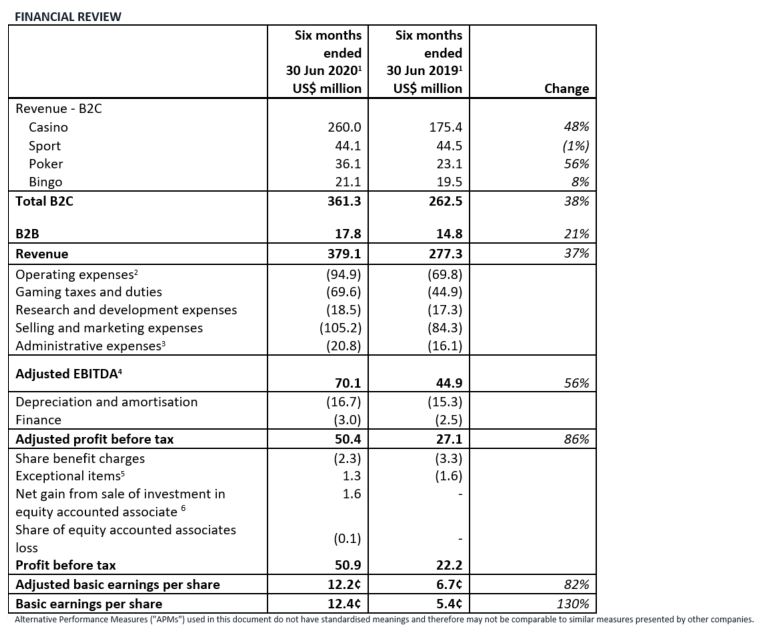

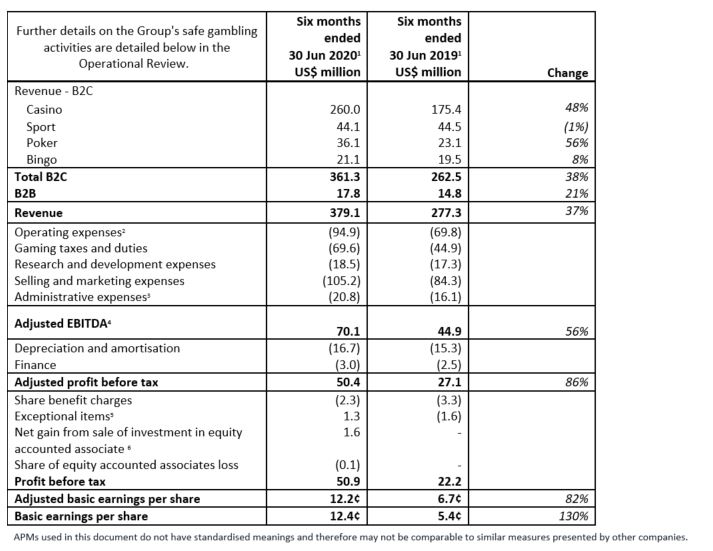

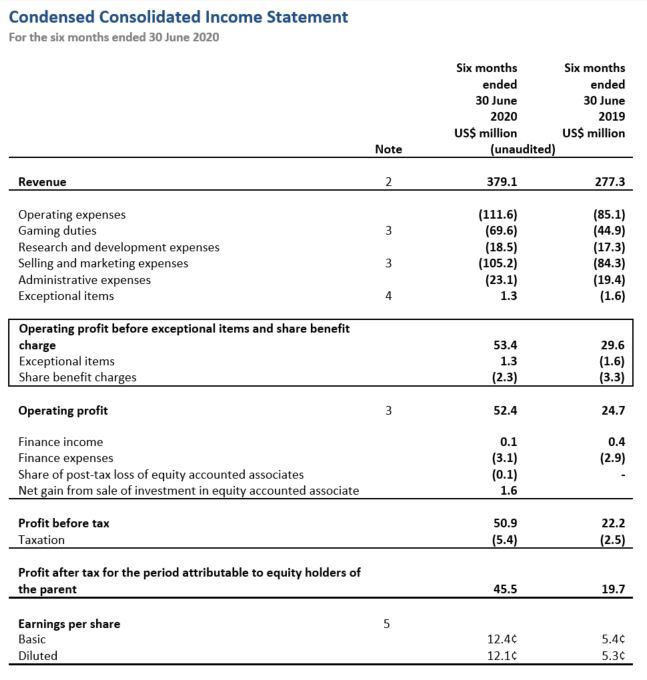

- Group revenue increased 37% to US$379.1 million (H1 2019: US$277.3 million).

o B2C Revenue increased 38% to US$361.3 million (H1 2019: US$262.5 million);

- Casino revenue increased 48% to US$260.0 million (H1 2019: US$175.4 million);

- Poker revenue increased 56% to US$36.1 million (H1 2019: US$23.1 million);

- Sport revenue decreased 1% to US$44.1 million (H1 2019: US$44.5 million); better than expected customer reaction to the gradual return of sports events in the summer with Sport revenue during June 59% ahead of the prior year;

- Bingo revenue increased 8% to US$21.1 million (H1 2019: US$19.5 million);

o B2B revenue increased 21% to US$17.8 million (H1 2019: US$14.8 million);

- Revenue from regulated and taxed markets represented the significant majority of Group revenue at 73% (H1 2019: 74%).

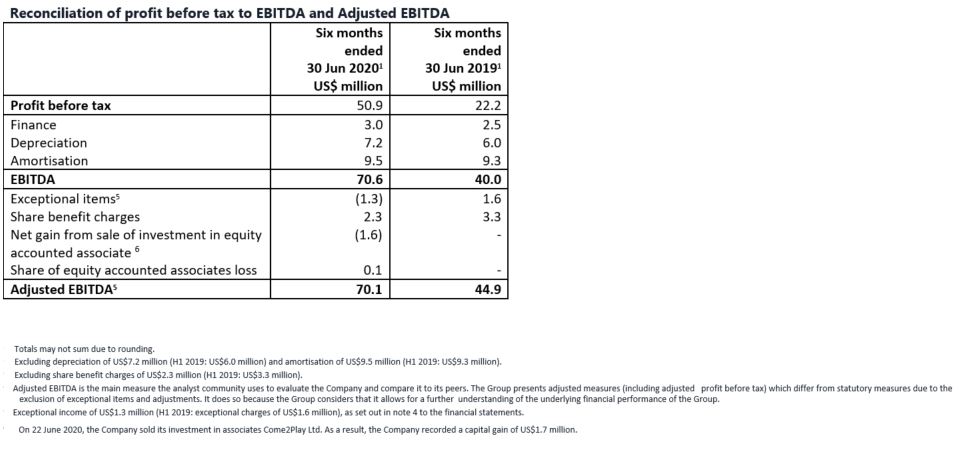

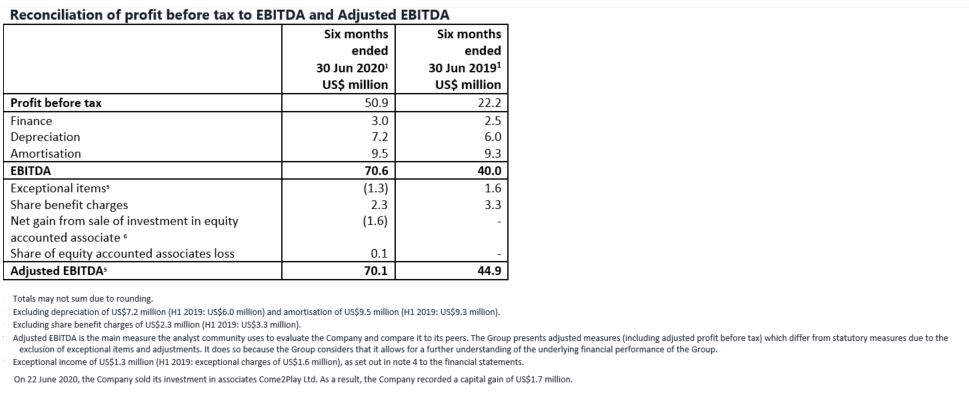

Adjusted EBITDA increased 56% US$70.1 million (H1 2019: US$44.9 million); the Adjusted EBITDA margin was 18.5% (H1 2019: 16.2%); EBITDA for the period amounted to US$72.1 million (H1 2019: US$40.0 million).

- Profit before tax increased 130% to US$50.9 million (H1 2019: US$22.2 million); Adjusted Profit before tax was US$50.4 million (H1 2019: US$27.1 million).

- Basic earnings per share increased to 12.4¢ (H1 2019: 5.4¢ per share); Adjusted basic earnings per share was 12.2¢ (H1 2019: 6.7¢).

- Interim dividend of 3.2¢ per share (H1 2019: 3.0¢ per share) plus an additional one-off 2.8¢ per share bringing the total to 6.0¢ per share.

Operational Highlights

- Increased vigilance on safe gambling and preventing gambling-related harm during COVID-19 period including:

o New algorithms introduced to our Observer system;

o Targeted communication to ensure customers continued to enjoy safe gambling across our brands;

o Re-launched “Too much is too much” safer gambling campaign to continue to develop awareness to the risks associated with excessive gambling;

o During H1, we more than doubled safe gambling interactions with customers.

- First time depositors (‘FTDs’) across the Group’s B2C brands increased 49% year on year:

o Casino FTDs increased 72%;

o Poker FTDs increased 103%.

- Successful launch of proprietary sportsbook platform in Sweden in April 2020 with the UK planned by early 2021.

- Strong momentum in the US with revenue increasing by 90% year-on-year reflecting significant B2C growth in New Jersey.

Current Trading

- During the third quarter to-date* 888 has continued to trade ahead of the Board’s expectations with average daily revenue 56 % higher than the prior year. This performance reflects the Group’s high levels of customer acquisition during the year to date as well as the benefit from the structural shift towards online services that has accelerated across several consumer-facing industries during recent months. As a result, the Board now anticipates that 888 will achieve an adjusted EBITDA outcome for 2020 significantly ahead of its prior expectations.

* Period from 1st July 2020 to 28 September 2020.

Post period end highlights

- In September the Group announced the appointment of Yariv Dafna as the Group’s new CFO on 1 November 2020. This appointment follows the Group’s announcement on 14 January 2020 that, after more than 15 years as Group CFO, Aviad Kobrine is stepping down from the role.

- In September the Group announced the appointment of Lord Jonathan (Jon) Mendelsohn as a Non-Executive Director and Chair Designate with immediate effect. Following a handover period to ensure a smooth transition of responsibilities, Jon will succeed Brian Mattingley as Chair of the Board when Brian stands down from the Group at the next Annual General Meeting in May 2021.

Itai Pazner, CEO of 888, commented:

“888 has performed very well throughout the first half of 2020 with robust year-on-year growth in revenue and Adjusted EBITDA of 37% and 56% respectively. This outcome reflects the Group’s continued strong levels of customer acquisition, general consumer trends towards increased use of online services especially during the COVID-19 lockdown period and 888’s relentless focus on product leadership.

We recognised early on that the COVID-19 pandemic would have a material impact on the lives of our customers across many global markets and this required an appropriate response from 888. We were therefore quick to increase our vigilance on safe gambling and preventing gambling-related harm.

We are pleased with our continued progress in the US where revenue increased by 90% year-on-year reflecting the Group’s outstanding B2C growth in New Jersey as well as strong performances from our B2B partners. We remain excited by the potentially significant medium-to-long-term opportunities for 888 in the US market.

888 is looking forward to delivering further product enhancements including the introduction of our new poker product across markets during H2 2020 and the launch of our proprietary sportsbook in the UK early next year. In addition, we are continuing to invest in safe gambling tools and will begin the roll-out of a new customer-centric safe gambling feature called the ‘Control Centre’ later this year that will offer customers an improved interface to help them understand better their gambling behaviour.

As a result of the Group’s continued momentum, as well as its strengths as a product-centric, responsible and diversified operator, the Board believes that 888 has a unique platform to deliver continued strategic progress during H2 and beyond.”

Itai Pazner, Chief Executive Officer, and Aviad Kobrine, Chief Financial Officer, will host a presentation for sell-side analysts today at 10:00 (BST). Please contact [email protected] or call +44 (0)207 796 4133 for further details.

A replay will be available from the investor relations section of 888’s website (http://corporate.888.com/investor-relations) later today.

Enquiries and further information:

This announcement includes statements that are, or may be deemed to be, “forward-looking statements”. By their nature, forward-looking statements involve risk and uncertainty since they relate to future events and circumstances. Forward-looking statements may and often do differ materially from actual results. Any forward-looking statements in this announcement reflect 888’s view with respect to future events as at the date of this announcement. Save as required by law or by the Listing Rules or the Disclosure Guidance and Transparency Rules of the UK Listing Authority, 888 undertakes no obligation publicly to release the results of any revisions to any forward-looking statements in this announcement that may occur due to any change in its expectations or to reflect events or circumstances after the date of this announcement.

INTRODUCTION

888 has performed well throughout the first half of 2020 with year-on-year growth in revenue and Adjusted EBITDA of 37% and 56% respectively. This outcome reflects the Group’s strong levels of customer acquisition during H2 2019; increased consumer demand for online services especially during the COVID-19 lockdown period; the Group’s diversification across product verticals and geographic markets; and the skill and commitment of 888’s global teams.

As a result of the Group’s continued momentum, as well as its strengths as a product-centric, responsible and diversified operator, the Board believes that 888 has a strong platform to deliver continued growth in the second half of financial year compared to H2 2019 and generate further shareholder returns.

COVID-19 impact

The outbreak and spread of COVID-19 during H1 2020 created an unprecedented environment for communities, businesses and consumers across the world. Our priority throughout this period has been on protecting the wellbeing of our colleagues and customers.

As countries across the world went into lockdown, we were quick to implement our business continuity plan which included making improvements to our technological infrastructure, priming of operational teams for emergency support, implementing work-from-home processes, and communicating clearly and constantly with employees. I would like to thank all my colleagues around the world for their flexibility and dedication throughout this challenging period. I am incredibly proud of how 888 has not only risen to this unique set of challenges over recent months but also managed to deliver a performance ahead of our initial expectations for the period and achieve further outstanding strategic progress.

COVID-19 has also had a material impact on the lives of our customers across many global markets. Restrictions on people’s movements and leisure activities has accelerated the ongoing structural shift towards online services across multiple consumer-facing industries. As a purely online operator, 888 remains well positioned to continue to benefit from this shift.

Safer. Better. Together: protecting customers during the pandemic

We recognised early in the COVID-19 pandemic that, with people spending more time at home and with potentially increased levels of stress, our vigilance on safe gambling and preventing gambling-related harm was even more important than ever. The Group acted swiftly in accordance with this responsibility as follows:

- We proactively introduced new algorithms to our Observersystem – our proprietary software which monitors every customer’s deposits, withdrawals, bets, and communications to identify behaviours that may be a potential risk. These new features identified and flagged potential warning signs as a result of increases in a customer’s activity during the lockdown period and, where relevant, prompted intervention from our expert safer gambling team.

- We ensured that no customer communications included incentives which may be related to COVID-19.

- We conducted a programme of targeted communication to ensure our customers continue to enjoy safe gambling across our brands. This has involved proactive emails to all customers about how to stay in control of their gambling during the lockdown period.

- We re-launched our “Too much is too much” safer gambling campaign on social media to continue to develop awareness to the risks associated with excessive gambling.

- During H1, we significantly increased the volume of interactions our safer gambling team initiated with customers and more than doubled the number of accounts upon which we placed restrictions in order to protect customers’ wellbeing. This reflected our more cautious approach to monitoring player affordability.

- At a global level, we continue to pool learnings from around the world to deliver a safe environment for our players. In addition, we have fully complied with special measures brought into effect by regulators in Spain and Sweden during the pandemic.

- In the UK, we temporarily froze all bonus offers to any customers who are displaying indicators of harm and prevented all customers from reversing withdrawals from our sites. In addition, our safer gambling team has conducted an ongoing review of relevant customers to ensure that they continue to gamble safely and that their financial situation has not altered since the beginning of the pandemic.

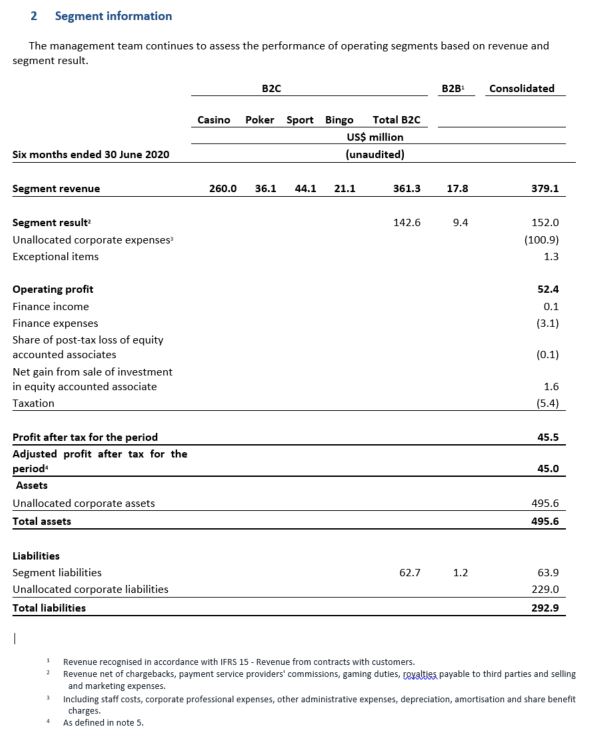

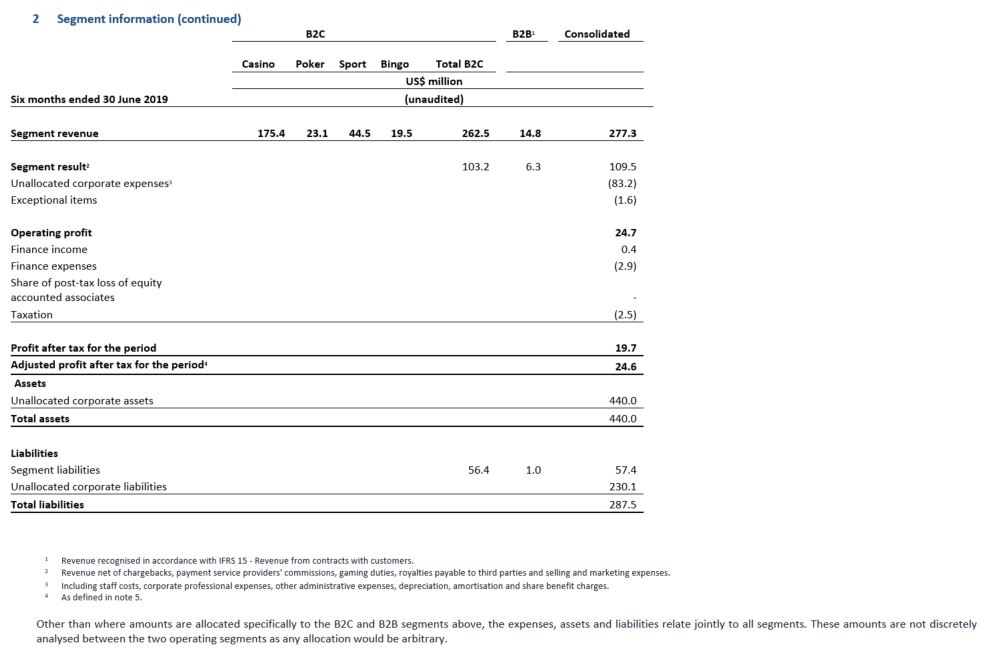

Revenue

Group revenue increased by 37% to US$379.1 million (H1 2019: US$277.3 million). This was driven by a 38% increase in B2C revenue which reflected the Group’s continued momentum across several regulated markets during the period. This outcome was led by the particularly strong performances of Casino and Poker which recorded revenue growth of 48% and 56% respectively. These positive results were partly offset by a 1% decline in Sport revenue reflecting the COVID-19-related cancellation and suspension of sporting events across the globe from March to June. At constant currency, however, Sport revenue increased 2% despite the impact of COVID-19 reflecting: a strong performance in Q1’20; a recovery and strong performance during June; and actions taken by management to provide a relevant sport offering throughout the lockdown period. B2C Bingo revenue increased by 8% (flat on a pro forma1 basis). B2B revenue increased by 21% to US$17.8 million (H1 2019: US$14.8 million) as a result of: good progress across the Group’s Bingo B2B network; growth in Delaware through our state lottery partnership; and a strong performance by our WSOP (World Series of Poker) partner in the US.

In line with the Group’s strategic focus and reflecting its progress across several regulated markets including Sweden and Portugal, where 888 launched during the prior year, the proportion of revenue generated from regulated markets increased by 2% to 64% (H1 2019: 62%). The proportion of revenue generated from regulated and taxed markets decreased to 73% of Group revenue (H1 2019: 74%), as a result of lower share of revenue from Germany at 4.6% (H1 2019: 6.0%).

1 Excluding the acquired Jet Bingo brands and at constant currency.

Operating Expenses

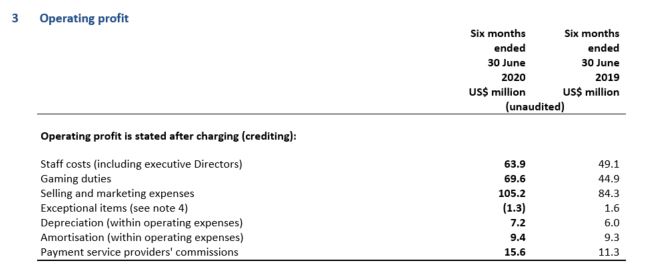

Operating Expenses2 increased by 36% to US$94.9 million (H1 2019: US$69.8 million) with the ratio of Operating Expenses to revenue decreased to 25.0% (H1 2019: 25.2%). The increase in Operating Expenses is explained by the continued growth of Casino revenue which resulted in higher royalty charges payable to third-party game providers, higher commissions payable to payment service providers and costs related to operational risk management services which resulted from the increased activity during the period. Reported Operating Expenses amounted to US$111.6 million (H1 2019: US$85.1 million).

2 Excluding depreciation of US$7.2 million (H1 2019: US$6.0 million) and amortisation of US$9.5 million (H1 2019: US$9.3 million).

Gaming taxes and duties

Gaming duties increased by 55% to US$69.6 million (H1 2019: US$44.9 million). This is a result of the Group’s strong revenue growth in several regulated markets. In addition, the Remote Gaming Duty rate in the UK increased from 15% to 21% of Gross Gaming Revenues effective from April 2019 resulting in incremental duties of US$4.0 million in the period and the gaming tax rate in Portugal increased from 15% to 25% effective from April 2020.

Research and development expenses

Research and development (‘R&D’) expenses increased by 7% to US$18.5 million (H1 2019: US$17.3 million). During the period, the Group invested in further developing the Sport platform that was acquired in March 2019 as well as the development of new products, games and features that further enhance customer experience, with a continued emphasis on safe gaming and customer protection. Reflecting the revenue growth during the Period, the ratio of R&D expenses to revenue declined to 4.9% (H1 2019: 6.2%).

Selling and marketing expenses

Selling and marketing expenses as a proportion of revenue decreased to 27.7% (H1 2019: 30.4%) reflecting the Group’s revenue growth during the period and 888’s responsible approach to marketing during the COVID-19 pandemic. Selling and marketing expenses increased by 25% to US$105.2 million (H1 2019: US$84.3 million), however, this increase was primarily due to a rise in customer engagement rates with online advertisements for which 888 pay per click rather than increased investment to broaden the reach of the Group’s marketing activity. B2C first time depositors increased by 49% and cost per new customer acquisition declined, in part reflecting the continued effectiveness of the Group’s strict returns-driven marketing approach.

Administrative expenses

Administrative expenses1 amounted to US$20.8 million (H1 2019: US$16.1 million) mainly reflecting increases in legal, regulatory and tax advice in line with the growing complexity of the Group’s regulatory footprint. Reported administrative expenses amounted to US$23.1 million (H1 2019: US$19.4 million). In addition, due to economies of scale the ratio of administrative expenses to revenue declined to 5.5% (H1 2019: 5.8%).

1 Excluding share benefit charges of US$2.3 million (H1 2019: US$3.3 million)

Adjusted EBITDA

Adjusted EBITDA for the period increased 56% to US$70.1 million (H1 2019: US$44.9 million). The Adjusted EBITDA margin expanded to 18.5% (H1 2019: 16.2%) reflecting the strong revenue growth and operational gearing in both marketing and operating expenses. Operational gearing was driven by the Group’s strict cost control throughout the period as well as its continued return-on-investment approach to marketing investment. EBITDA for the period amounted to US$70.6 million (H1 2019: US$40.0 million).

Exceptional items

Exceptional income of US$1.3 million (H1 2019: exceptional expenses of US$1.6 million) was recognised during the period. During this period, while assessing a past provision in respect of regulatory matters, management concluded that the balance should be reduced by US$2.8 million. The remaining provision balance represents management’s best estimate of probable cash outflows related to these matters, which are closely monitored by the Group. In addition, the Group recognised a provision of US$1.5 million arising from a regulatory related matter which arose following period end.

Share benefit charges

The Group recorded a share benefit charge of US$2.3 million (H1 2019: US$3.3 million) mainly attributed to long-term incentive equity awards granted to eligible employees.

Finance income and expenses

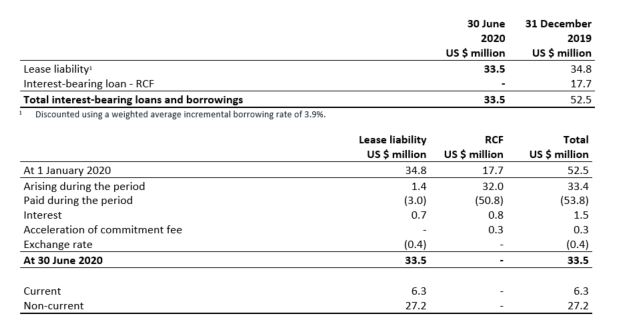

Finance expenses were US$3.1 million (H1 2019: US$2.9 million). This comprised: non-cash interest expenses of US$0.7 million related to IFRS 16, US$1.5 million non-cash currency exchange differences and US$0.8 million interest charge in respect of RCF loan which was fully re-paid during the period. Finance income amounted to US$0.1 million (H1 2019: US$0.4 million). Net finance expenses amounted to US$3.0 million (H1 2019: US$2.5 million).

Profit before tax

Profit before tax increased to US$50.9 million (H1 2019: US$22.2 million) mainly as a result of higher EBITDA as described above. Adjusted Profit before tax was US$50.4 million (H1 2019: US$27.1 million).

Taxation

Taxation for the period was US$5.4 million (H1 2019: US$2.5 million) as a result of the higher profit generated in the period.

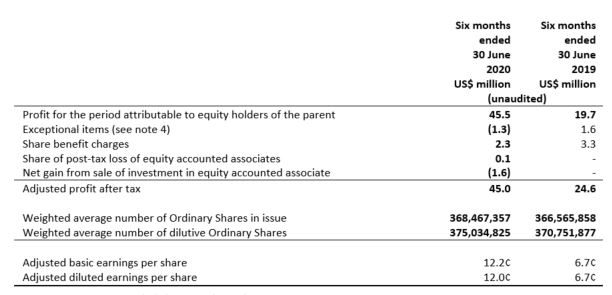

Adjusted Profit after tax and Profit after tax

Adjusted profit after tax1 was US$45.0 million (H1 2019: US$24.6 million). Profit after tax was US$45.5 million (H1 2019: of US$19.7 million).

1 As defined in note 5 to the H1 2020 financial statements.

Earnings per share

Basic earnings per share increased to 12.4¢ (H1 2019: 5.4¢ per share). The increase is a result of higher Profit after tax during the period. Adjusted basic earnings per share was 12.2¢ (H1 2019: 6.7¢). Further information on the reconciliation of adjusted basic earnings per share is provided in Note 5 to the H1 2020 financial statements.

Dividend

The Board has declared an interim dividend of 3.2¢ per share in accordance with 888’s dividend policy, plus an additional one-off 2.8¢ per share, bringing the total to 6.0 ¢ per share (H1 2019: 3.0¢ per share) reflecting the strong performance of the Group during the first half of the year, 888’s continued strong current trading and cash generation as well as the Board’s continued confidence in its outlook.

Cash flow

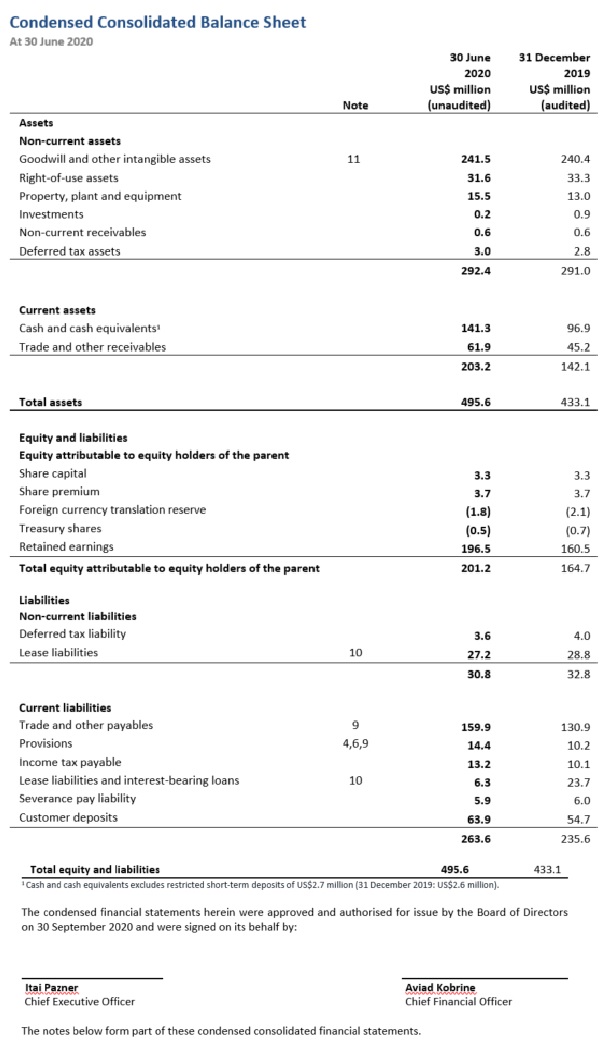

Net cash generated from operating activities increased 120% to US$94.2 million (H1 2019: US$42.7 million) as a result of the strong results during the period.

Net cash used in investing activities was US$16.9 million mainly includes acquisition of property, plant and equipment of US$6.6 million and internally generated intangible assets of US$8.9 million (H1 2019: US$64.6 million mainly includes the acquisition of the BetBright sport platform, Costa Bingo brands and AAPN Holdings LLC).

Net cash used in financing activities was US$33.1 million (H1 2019: US$0.9 million) related to the repayment of RCF loan in the net amount of US$18.0 million (H1 2019: proceeds from RCF loan of US$33 million). At the end of the period the RCF remained undrawn in its entirety. Dividend payments during the period amounted to US$11.1 million (H1 2019: US$29.4 million).

Balance sheet

The Group held cash at 30 June 2020 of US$141.3 million (31 December 2019: US$96.9 million)1. The increase in the cash balance is primarily a result of the strong cash flow generated from operating activities. Balances owed to customers were US$63.9 million (31 December 2019: US$54.7 million).

In February 2019, 888 signed an RCF with Barclays Bank plc enabling the Group to borrow an amount of up to US$50 million. During May 2019 the Group drew down US$33 million in order to provide short term finance for its M&A activities. During the period to 30 June 2020, following the increase in cash balance the Group repaid the full RCF loan.

1 Cash balance excludes restricted short-term deposits of US$2.7 million (31 December 2019: US$2.6 million).

OPERATIONAL REVIEW

888’s growth strategy is aimed at achieving the Group’s potential across a diverse range of geographic markets by delivering organic growth in a responsible manner as well as evaluating attractive M&A opportunities. Underpinning this strategy are 888’s core strengths including product development, business analytics, customer relationship management and marketing. 888 made continued progress against each of the following key areas of its growth strategy during H1 2020:

Continue to protect customers and act responsibly

888 firmly believes that providing a safe environment for customers is not only the right thing to do but puts the Group in a stronger position to continue generating long-term value for all stakeholders. In addition to the stricter safe gambling measures introduced during the pandemic described above, we continued to focus on delivering our safe gambling strategy, which we call Safer. Better. Together. and is outlined in more detail in the Group’s 2019 Annual Report.

During the period we continued to actively participate in the UK Gambling Commission’s industry groups on game design and incentives for high value customers-the latter of which released a proposed code of practice for wider consultation in June. 888 is committed to applying the outcomes of these consultations to its own safer gambling measures where such actions have not already been taken.

Empowering our customers to gamble safely has remained a core component of our new product development initiatives. During the period we continued to develop our Control Centre, a new safe gambling feature, ahead of its planned roll-out later in 2020. The Control Centre will sit across each of 888’s websites and will provide customers with an improved interactive interface to help them understand better their gambling behaviour and will further increase the prominence of 888’s safer gambling tools at all times.

Understanding each customer’s “affordability” to gamble is a key part of 888’s safe gambling strategy. During the period, in addition to the measures outlined above, we have been participating in the Betting and Gaming Council -led affordability working group and have applied enhanced levels of customer due diligence on an ongoing basis.

Development of 888’s core B2C business

The Group has ambitious targets to develop its core B2C business with a strategic focus on expanding 888’s presence amongst recreational customers across regulated markets globally. 888 continues to develop leading brands across four major online gaming verticals (casino, sport, poker and bingo) by focusing on providing a safe and enjoyable online gaming entertainment experience for customers.

During the period, B2C Revenue increased by 38% to US$361.3 million (H1 2019: US$262.5 million). In addition, 888 increased B2C first-time depositors (‘FTDs’) by 49% year-on-year. The Group’s progress was driven by expansion across its key markets, further progress in Casino, a strong recovery in Poker and the structural shift towards online entertainment during the COVID-19 pandemic.

Casino – continued progress towards being the global brand leader

Casino revenue increased by 48% to US$260.0 million (H1 2019: US$175.4 million). Casino first time depositors increased by 72%. We are delighted that our continued product innovation and subsequent progress has again been recognised with 888Casino named winner in the 2020 Gaming Intelligence Award’s Casino Operator of the Year category.

Poker – return to growth reflecting strong entertainment proposition

Poker revenue increased significantly by 56% to US$36.1 million (H1 2019: US$23.1 million). Poker first time depositors more than doubled with an increase of 103%. The Group’s strong Poker results benefited from continued investment in 888’s poker product; and the launch of the Group’s shared player liquidity network between Spain and Portugal during 2019. Poker remained an important customer acquisition channel for the Group with 24% of the Group’s B2C first time depositors during the period acquired through the Poker vertical. The flow of poker players also playing Casino and Sport continued to be an important element of the B2C business.

888 is focused on building on its strong H1 performance in Poker and maintaining its established position as a top-three online poker brand globally with strong appeal amongst recreational poker players. To support this, the Group is continuing to deliver new product enhancements and, during the second half of the year, is progressing the roll-out of its Poker 8 platform across markets with encouraging initial results so far.

Sport – short-term COVID-19 disruption but encouraging momentum as sporting events returned

888’s Sport performance during the period was impacted by the COVID-19-related suspension and cancellation of sporting events from March. Prior to this disruption, Sport revenue in January and February was up 22% year on year. During the lockdown period many customers found interest in traditionally less popular events and categories such as e-sports, Virtual Sports, Darts and Table tennis. In addition, 888 saw a better than expected customer reaction to the gradual return of sports events in the summer and Sport revenue during June was 59% ahead of the prior year. Overall Sport revenue during the period was resilient and decreased by only 1% to US$44.1 million (H1 2019: US$44.5 million) representing an increase of 2% at constant currency. Sport first time depositors decreased by 3%.

The Group’s ambition is to continue to develop 888sport as a leading online sportsbook operator across global regulated markets. The Group was pleased to succesfully launch its proprietary sportsbook platform in Sweden during April 2020 and we remain excited by the long term growth opportunities that having ownership of a proprietry end-to-end sports product will offer the Group. We now plan to roll-out the new platform into additional markets with the UK planned by early 2021.

Bingo – good growth reflecting “value-for-time” entertainment offering

B2C Bingo recorded revenue growth of 8% to US$21.1 million (H1 2019: US$19.5 million). This performance benefited from the contribution of the enlarged portfolio of acquired brands in mid-March 2019. On a pro forma basis, Bingo revenue was flat year-on-year reflecting low gaming margins in the first quarter of the year. Encouragingly, deposits, active players and new customers acquisition all increased during the period. Customer acquisition saw a 43% increase (26% increase pro forma), building a healthy customer base going into the second half of the year.

Expansion in attractive regulated markets

888’s strategic focus remains on growing in sustainable, regulated markets where the Group can leverage its full marketing expertise to capture opportunities. Revenue from regulated and taxed markets continued to represent the majority of Group revenue at 73% (H1 2019: 74%).

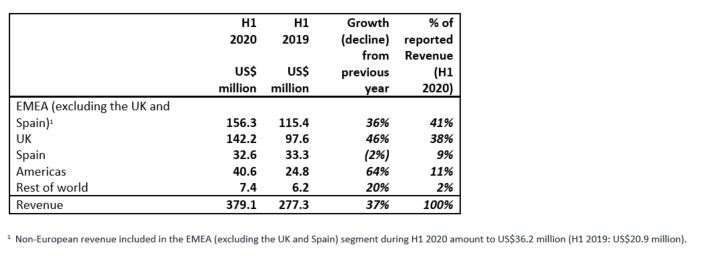

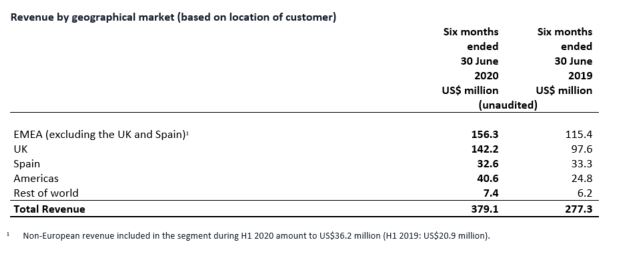

The table below shows the Group’s revenue by geographical market:

EMEA (excluding the UK and Spain)

Revenue from EMEA (excl. the UK & Spain) increased 36% during the first half of 2020. This was driven by growth in Casino and Poker across multiple markets offset in part by the Group’s overall Sport performance which was impacted by the COVID-19 related cancellation of sports events.

Italy delivered continued strong revenue growth of 51% reflecting encouraging performances in Casino and Poker. Casino revenue in Italy increased by 52% and Poker revenue increased by 141%. 888.it delivered an overall 41% increase in first time depositors during the period despite the strong comparatives in H1 2019 and the lack of sporting events.

The Group continued to perform well in Romania where revenue increased by 111% and first-time depositors increased by 250%.

The Group continued to expand in Sweden where it launched regulated Sport, Casino and Poker in January 2019. Revenue from Sweden increased by 123% during the period. As outlined above, we were also pleased to launch our Spectate proprietary sportsbook platform in Sweden in April and have been encouraged by the customer feedback and reaction following the resumption of major sports events since June.

We are pleased with our progress in Portugal where we launched 888casino in January 2019 and 888poker in July 2019. The launch of Poker in Portugal enabled the Group to establish its first European interstate poker network to pool poker players across the Spanish and Portuguese markets. We are pleased with both our customer acquisition in Portugal and the improved Poker performance in Spain which nearly doubled revenue during the period, despite marketing limitations imposed by the Spanish regulator during the COVID-19 lockdown.

Although revenue from Germany increased during the period, the performance was held back as a result of restrictions on and the withdrawal from the market of certain payment providers. As a result, the share of Group revenue from this market decreased to 4.6% (H1 2019: 6.0%).

UK

UK revenue increased during the period to US$142.2 million (H1 2019: US$97.6 million). The UK represented 38% (H1 2019: 35.2%) of Group revenue. The Group continues to invest in entertaining recreational customers with new product features focused on casual and safer play. UK Sport revenue recovered with the resumption of major sporting events and in June achieved strong growth of 148% year-on-year.

The Group’s predominantly UK-focused Dragonfish bingo network continued its progress in part due to the success of its new customer interface (known internally as SnowWhite) inspired by 888’s successful Orbit Casino platform. The SnowWhite interface has enhanced the customer experience, integrated additional marketing functionality and improved safe gaming monitoring. By the period end, the Group had deployed all its B2B Bingo skins on to the new SnowWhite platform.

Spain

Revenue from Spain decreased by 2% to US$32.6million (H1 2019: US$33.3 million). Revenue growth of 91% in Poker and 6% in Casino was offset by a decline of 41% in Sport due to the cancellation of sporting events. First time depositors during the period increased by 18% in Casino and by 51% in Poker. Spain represented 9% of Group revenue during the period (H1 2019: 12.0%). As with other European markets, Sport revenue in Spain in June started to recover with the resumption of some major sporting events.

Americas

Revenue from Americas increased by 64% to US$40.6 million (H1 2019: US$24.8 million). US revenue increased by 90% year-on-year. This primarily reflected the Group’s strong B2C growth in the New Jersey market, driven by the investments made in 888’s product in the US market over recent periods. New Jersey B2C revenue increased by 85% and first-time depositors in the state increased by 76%.

The Group’s B2B business in the US market also achieved pleasing results with strong performances in Delaware through the Group’s partnership with the Delaware lottery and by the Group’s WSOP (World Series of Poker) partner across Delaware, Nevada and New Jersey.

The Group remains focused on investing to deliver the significant medium-to-long-term growth opportunities for 888 in the US market. In June, 888 was pleased to announce a two-year extension to its exclusive iGaming contract with the Delaware Lottery and the Group continues to appraise opportunities to provide both brand building and market access for 888 in the developing North American online gaming market.

Non-US revenue increased by 57% year-on-year primarily reflecting the Group’s strong B2C Casino and Poker activity during the period.

Enhancing efficiencies

The Board and 888’s management team have maintained focus on maximising operational efficiencies and maintaining tight cost control.

The 49% increase in new customers was achieved despite a lower ratio of marketing spend to revenue. This was in part driven by increased demand for the Group’s services during the lockdown period and also reflected the Group’s continued focus on highly efficient marketing investment. During the period the Group also invested in enhancing its technological infrastructure to support more efficient remote working moving forward.

Board & Team

In July, post the period end, we were pleased to announce the appointment of Limor Ganot as an independent non-executive director, effective 1 August 2020. Limor’s involvement as a leader in a diverse range of businesses, together with her understanding of disruptive technologies, will be of significant benefit to 888 as we continue to grow and develop as a global leader in online gaming.

In September, post the period end, the Group announced the appointment of Yariv Dafna as the Group’s new CFO. This appointment follows the Group’s announcement on 14 January 2020 that, after more than 15 years as Group CFO, Aviad Kobrine is stepping down from the role. Yariv will join the Group on 1 November 2020 and be appointed to the Board on the same date. Aviad will step down from the Board on the same date.

In September, the Board was delighted to announce the appointment of Lord Jonathan (Jon) Mendelsohn as a Non-Executive Director and Chair Designate with immediate effect. Jon is a highly experienced gambling sector professional with more than 20 years’ industry experience that includes co-founding Oakvale Capital LLP, a leading M&A and strategic advisory boutique focusing on the gaming, gambling and sports sectors. Jon is a Labour life peer who has sat in the House of Lords since October 2013 and sits on the International Relations and Defence Committee. Following a handover period to ensure a smooth transition of responsibilities, Jon will succeed Brian Mattingley as Chair of the Board when Brian stands down from the Group at the next Annual General Meeting in May 2021.

Going concern

Following a review of the Group’s forecasts and its access to financing, the Directors have a reasonable expectation that the Group has adequate resources to continue in operational existence for the foreseeable future. Therefore, the Directors continue to adopt the going concern basis in preparing these interim financial statements. Further detail on the considerations of the Directors is given in Note 1.1.

Current trading and outlook

During the third quarter to-date* 888 has continued to trade ahead of the Board’s expectations with average daily revenue 56% higher than the prior year. This performance reflects the Group’s high levels of customer acquisition during the year to date and the benefit from the structural shift towards online services that has accelerated across several consumer-facing industries during recent months. As a result, the Board now anticipates that 888 will achieve an adjusted EBITDA outcome for 2020 significantly ahead of its prior expectations.

* Period from 1st July 2020 to 28 September 2020.

888 is looking forward to delivering further product enhancements including the roll-out of Poker 8 across markets in the second half of the year and the launch of Spectate, 888’s proprietary sports book platform, in the UK at the beginning of 2021. In addition, 888 remains highly vigilant about its responsibilities to continue to protect customers and prevent gambling-related harm and will begin the roll-out of a new customer-centric safe gambling feature called the “Control Centre” during the second half of the year.

While the Group has delivered a strong performance during the year to date, the Board remains mindful of possible future headwinds including the potential for a prolonged period of global macro-economic uncertainty that could impact consumers’ discretionary spending. Nevertheless, the Board remains confident that, underpinned by the Group’s unique technology and diversification across product verticals and geographic markets, 888 remains well positioned to deliver continued progress.

Principal risks and uncertainties

In addition to the risks faced by businesses generally and online businesses in particular, the Group is exposed to specific risks arising from its operations. The following key principal risks and uncertainties remain consistent with those included on pages 32-41 of the 2019 Annual Report and Accounts:

- Regulatory risk

- BREXIT-related risks

- Information Technology and cyber risks

- Taxation risk

- Retention of key personnel and succession risk

- Business disruption due to pandemics such as COVID-19

- Data protection risk

- Reputational risk

- Partnership risk

- Acquisition risks

- Liquidity risks

The Board has reconsidered and updated the description of the Group’s regulatory risk with respect to H1 2020 as follows:

In part as a response to the COVID-19 pandemic, various jurisdictions adopted a more stringent approach to player protection, primarily to avoid emergence of problem gambling patterns amongst those sheltering at home, and to curtail excessive spending on gambling during a period of economic downturn. In various jurisdictions this took the form of advertising restrictions, or the imposition of stricter player protection and responsible gambling measures, either temporarily or on a permanent basis. The UK’s Gambling Commission (“UKGC”) imposed various temporary responsible gambling measures in response to the COVID-19 pandemic, to curb the potential for increased spending and gambling addiction during lockdowns or by those sheltering at home. The Spanish Government imposed a prohibition on the offering of incentives or email and social media advertising during the COVID-19 lockdown. In Sweden, operators have been subject to temporary deposit limits for betting and online casino gambling, as well as an additional restriction on the maximum amount of bonuses.

The UKGC continued to take a strict approach towards compliance, tightening requirements, adopting more stringent policies and regulations, increasing the level of oversight over licensees and penalizing operators for failing to meet regulatory requirements and standards. The primary areas of focus for the UKGC continue to be responsible gambling and prevention of underage gambling, consumer protection, anti-money laundering, the use of proceeds of crime for gambling and the provision of full disclosure to the UKGC regarding ownership interests and holding structures. The UKGC adopted additional restrictions, e.g. a ban commencing in April 2020 on credit card transactions for gambling and stricter age verification obligations. The Commission has also proposed additional restrictions relating to the design of online slots, as well as standards applicable to player withdrawal requests. The Group continued to work closely with the UKGC on various initiatives, to update its policies and procedures and to strengthen internal reporting lines to ensure compliance within the business, investing significant resources in regulatory compliance measures. There continued to be calls, particularly within Parliament, for the imposition of stricter limitations on the advertising of gambling services, as well as ongoing criticism of the Gambling Commission’s treatment of the industry. The senior government officials responsible for the sector under the current British administration appear to have adopted a circumspect approach towards the industry, which may result in both restrictive legislation and regulation, and a further tightening of regulatory standards by the relevant authorities. By way of example, the Gambling Related All-Party Parliamentary Group continued to call for imposition of a GBP 2 staking limit for online gambling games (in line with the limit imposed on FOBTs), which may have prompted the proposed restrictions on online slot machines considered by the Commission. The same report advocated a ban on credit card gambling, a measure adopted by the UKGC in early 2020.

Another report by a non-partisan think-tank recently called for the imposition of a monthly cap on gambling losses, and for the imposition of tax penalties that would incentivize gambling operators to relocate onshore. In July 2020 the House of Lords Select Committee on the Social and Economic Impact of the Gambling Industry published a report containing various recommendation to reduce potential harm from gambling. These included testing of new games for the potential of addiction, imposition of restrictions on the speed of online games, imposition of affordability testing for players and the restriction of sports sponsorships. The House of Commons Public Accounts Committee also published a report criticizing the Gambling Commission and DCMS for its oversight of the gambling industry and measures adopt for protection of players and prevention of problem gambling.

In Germany, the Company is subject to prohibition orders issued by various German states, some have been upheld by German courts and others in the process of judicial review. While the Company continues to challenge the validity of these orders (where possible) before various courts, it has been consulting closely with its German advisers as to the appropriate operational measures to be taken by the Group in light of the orders issued. Germany’s regulatory landscape continues to undergo frequent and occasionally inconsistent changes. The Group along with many other operators continues to defend the legality of its services in Germany on various fronts, primarily with regard to states seeking to issue or enforce prohibition orders directed at the Group’s services within such states, and with respect to attempts by the German authorities to block financial transactions related to gambling services. On 1 January 2020, an amendment to the Interstate Treaty on Gambling came into force, introducing a federal licensing scheme for sports betting, representing a significant departure from previous iterations of the Treaty and previous attempts to introduce regulatory reform. The licensing regime imposes certain restrictions with respect to the available offering (specifically – a monthly stake limit, limitations on live betting and advertising restrictions) and also requires licensees to make certain undertakings with respect to their group’s operations with respect to the German market. The Group applied for a license under the new regime. As part of its license application, 888 was required to undertake not to offer or broker any form of “unlawful gambling” once issued a license, wording intended to capture casino gambling. The Group is evaluating with its German counsel the validity of such an undertaking, its practical ramifications once a license has been issued, and any means available to mitigate its impact. The licensing process has been indefinitely suspended by a German court and it is unclear whether it will eventually be implemented. Also in 2020 the 16 German states agreed on a sweeping reform to the regulatory landscape, scheduled for mid-2021, which would see the introduction of a federal licensing regime for sports betting and certain casino products (primarily online slots) and poker. This reform is conditional on its ratification by 13 of the 16 German states, and would represent a departure from the historical ban on online casino. As part of the reform, Germany may also adopt a temporary “toleration regime” which would allow online casino operators to offer their services prior to the introduction of full licensing, on the condition that they adhere to certain compliance requirements. Many details pertaining to the new permanent and temporary regimes are yet to be confirmed, and therefore the commercial appeal of this opportunity and its overall impact is presently difficult to evaluate. As presently worded, the amended Treaty would allow operators to offer “arcade-style” online slot machines, which would be subject to 1 euro stake limits and restricted play options. Other types of casino games (e.g. table games) would be regulated on a state by state basis and remain within the state lottery’s monopoly or subject to a restrictive concession model. The new Treaty would also impose a EUR 1,000 Euro monthly deposit limit that would apply across all operators (it is not clear yet how this would be implemented in practice).

In the Netherlands, where a law was approved in February 2019 to liberalize the market, the local regulator continues to take a proactive and strict approach towards enforcement of existing laws against operators whose operations are conducted in violation of the “prioritization criteria” for enforcement issued by the authorities, and which were updated with additional criteria during 2019. Several operators received significant fines due to the conduct of operations in a manner violating these criteria. Ambiguity lingers regarding the application of “bad actor” language in the new law, both in terms of timeline and in terms of scope. Operators who offered their services in the market prior to the licensing regime may be barred from participating in the liberalized market or have their eligibility for licensing delayed under a so called cool-off regime. Due to various delays in the legislative process, it appears unlikely that the Dutch regime will launch at the beginning of 2021 as was previously anticipated. 888 continues to adhere to the regulator’s criteria, as updated from time to time, and to follow developments on the regulatory front.

In Sweden, the Group began operating under a local license in 2019. The Swedish regulator has shown itself to be strict and proactive in enforcing regulatory standards and has on occasion informed the industry of its position on compliance by penalizing operators it perceived as non-compliant. 888 has studied the regulator’s position and enforcement action closely to ensure that its operations are in-line with local requirements.

In January 2019, the US Department of Justice issued a legal opinion on the scope of the federal Wire Act, overturning a previous opinion from 2011, and finding that the Act applies to all forms of gambling (not only sports betting, as was concluded in the previous opinion). Later in the year, a New Hampshire federal court set aside the aforementioned memorandum and rejected its interpretation of the Wire Act on substantive grounds, reverting to the status quo ex ante. The DOJ has appealed the decision and a hearing on the matter took place in H1 2020. The justices of the appellate court appeared to be unsympathetic to the DOJ’s position, prompting speculation that the appeal would be unsuccessful. The case may eventually reach the US Supreme Court. The Group continues to follow developments on this front closely, to evaluate their impact on US operations and future growth.

In Italy, there have been calls to ease the advertising ban that came into force during 2019, as a way of reviving the Italian gambling industry as well as the Italian sporting industry following the COVID-19 downturn. In contrast, other European jurisdictions, most notably Spain, continue to mull the possibility of imposing similar restrictions on the advertising of gambling services. Spain notified the EC of a draft regulation severely restricting gambling advertising, which could come into force later in 2020.

From time to time, the Group is the target of claims or litigation from customers in unregulated jurisdictions seeking to recover losses based on arguments pertaining to the legality of the Group’s offering in their jurisdiction. The Group is currently seeing a growing trend of such claims.

Notes to the Condensed Consolidated Financial Statements

1 Basis of preparation and accounting policies

1.1 Basis of preparation

The condensed consolidated half-yearly financial information of the Group has been prepared in accordance with International Accounting Standard 34 ‘Interim Financial Reporting’ as adopted by the EU (‘IAS 34’) and with the Disclosure and Transparency Rules of the Financial Conduct Authority. The interim condensed consolidated financial statements do not include all the information and disclosures required in the Group’s annual audited consolidated financial statements and should be read in conjunction with the Group’s annual audited consolidated financial statements for the year ended 31 December 2019.

The financial information is presented in US Dollars (US$ million) because that is the currency the Group primarily operates in.

The comparatives for the year ended 31 December 2019 are not the Group’s full statutory accounts for that year. A copy of the statutory accounts for that year has been delivered to the Registrar of Companies in Gibraltar and is also available from the Company’s website. The auditor’s report on those accounts was unqualified and did not contain statements under Section 257(1) (a) and Section 258(2) of the Gibraltar Companies Act. A footnote to the Condensed Consolidated Balance Sheet describes a retrospective reclassification of items in the financial statements.

The condensed consolidated set of financial statements included in this half-yearly financial report has been reviewed, not audited, and does not constitute statutory accounts.

Further information relating to significant events during the period is provided in the Financial Review section.

Going concern

The Group closely monitors and carefully manages its liquidity risk. Base case cashflow forecasts are regularly produced which indicate that it will continue to have significant liquidity throughout the going concern period. Group management have run a downside scenario including the potential risk of a global economic slowdown. In the downside scenario, Group management have assumed variable cost savings proportional to the revenue reduction. As described above, trading during the second half of the financial year to date has been in line with recent trends supporting online consumption with average daily revenue 56% higher year on year and therefore the Directors consider the downside scenario to be remote. Following consideration of the base case forecast, the downside scenario, the Groups cash position and access to a financing in the form of a US$50 million revolving credit facility, the Directors have a reasonable expectation that the Group has adequate resources to continue in operational existence for the foreseeable future. Therefore, the Directors continue to adopt the going concern basis of accounting in preparing the interim financial statements.

1.2 New standards, interpretations and amendments adopted by the Group

The accounting policies and methods of computation adopted in the condensed consolidated half-yearly financial information are consistent with those followed in Group’s full financial statements for the year ended 31 December 2019, except for the adoption of new standards effective as of 1 January 2020.

Several new and amendments to existing International Financial Reporting Standards and interpretations, issued by the IASB and adopted by the EU, were effective from 1 January 2020 and have been adopted by the Group during the period with no significant impact on the consolidated results or financial position of the Group.

1.3 New standards that have not been adopted by the Group as they were not effective for the year:

Several new standards and amendments to existing International Financial Reporting Standards and interpretations, issued by the IASB and adopted, or subject to endorsement, by the EU, will be effective from 1 January 2021, 2022 and 2023 and have not been adopted by the Group during the period. At this stage management are still assessing the full impact on the consolidated results or financial position of the Group. None are expected to have a material impact on the consolidated financial statements in the period of initial application.

Geographical information

The Group’s performance can also be reviewed by considering the geographical markets and geographical locations within which the Group operates. This information is outlined below:

Notes to the Condensed Consolidated Financial Statements

4 Exceptional items

The Group classifies certain items of income and expense as exceptional, as the Group considers that it allows further understanding of the underlying performance of the Group. The Group considers any non-recurring items of income and expense for classification as exceptional by virtue of their nature and size.

Provision – regulatory matters

In 2018, the Group recorded a provision in respect of regulatory matters related to legacy customers’ activity in prior periods. During this period, while assessing these matters, management concluded that balance should be reduced by US$2.8 million. This amount represents management’s best estimate of probable cash outflows related to these matters, which are closely monitored by the Group. In addition the Group recognised a provision of US$1.5 million arising from a regulatory related matter which arose following period end.

Exceptional legal and professional costs

During H1 2019, the Group incurred legal and professional costs of US$0.8 million associated with the acquisitions of Jet Bingo brands and BetBright’s sports betting platform.

Restructuring costs

Restructuring costs in H1 2019 comprises with employees redundancy costs mainly in Israel, part of the Group cost optimisation project, shifting workforce from high cost locations to low cost locations.

5 Earnings per share

Basic earnings per share

Basic earnings per share (‘EPS’) has been calculated by dividing the profit attributable to ordinary shareholders by the weighted average number of shares in issue and outstanding during the period.

Diluted earnings per share

The weighted average number of shares for diluted earnings per share takes into account all potentially dilutive equity instruments granted, which are not included in the number of shares for basic earnings per share. Certain equity instruments have been excluded from the calculation of diluted EPS as their conditions of being issued were not deemed to satisfy the performance conditions at the end of the period or it will not be advantageous for holders to exercise them into shares, in the case of options. The number of equity instruments included in the diluted EPS calculation consist of 6,567,468 ordinary shares (H1 2019: 4,178,957) and nil market-value options (H1 2019: 7,062).

Adjusted earnings per share

The Directors believe that EPS excluding exceptional items, share benefit charges, share of post-tax loss of equity accounted associates and net gain from sale of investment in equity accounted associate (“Adjusted EPS”) allows for further understanding of the underlying performance of the business and assists in providing a clearer view of the performance of the Group.

Reconciliation of profit to profit excluding exceptional items, share benefit charges and share of post-tax loss of equity accounted associates and net gain from sale of investment in equity accounted associate (“Adjusted profit”):

6 Provisions, contingent liabilities and regulatory issues

(a) The Group operates in numerous jurisdictions. Accordingly, the Group files tax returns, provides for and pays all taxes and duties it believes are due based on local tax laws, transfer pricing agreements and tax advice obtained. The Group is also periodically subject to audits and assessments by local taxing authorities. Provisions for uncertain items are made using judgement of the most likely tax expected to be paid and the basis thereon, based on a qualitative assessment of all relevant information. The Board considers that any exposure for additional taxes, if any, that may arise from the final settlement of such assessments is unlikely to result in any further liability.

(b) As part of the Board’s ongoing regulatory compliance and operational risk assessment process, it continues to monitor legal and regulatory developments, and their potential impact on the business, and continues to take appropriate advice in respect of these developments.

Given the nature of the legal and regulatory landscape of the industry, from time to time the Group has received notices, communications and legal actions from a small number of regulatory authorities and other parties in respect of its activities. The Group has taken legal advice as to the manner in which it should respond and the likelihood of success of such actions. Based on this advice and the nature of the actions, for the majority of these matters the Board is unable to quantify reliably the outflow of funds that may result, if any. For matters where an outflow of funds is probable and can be measured reliably, amounts have been recognised in the financial statements within Provisions. Except for the regulatory matters described in note 9, these amounts are not material at 30 June 2020.

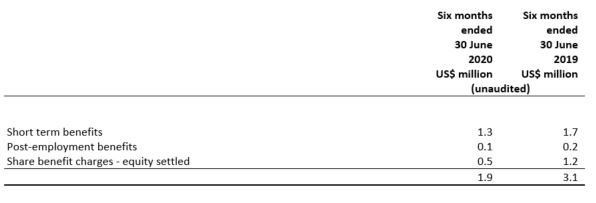

7 Related party transactions

The aggregate amounts payable to key management personnel, considered to be the directors of the Company, as well as their share benefit charges, are set out below:

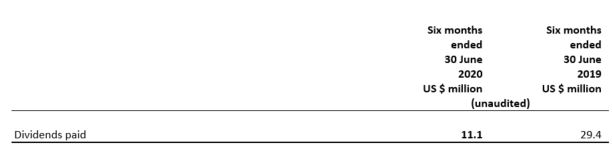

8 Dividends

2019 final dividend of 3.0¢ per share was paid on 22 May 2020 (US$11.1 million).

During 2019, the 2018 final dividend of 6.0¢ per share and an additional one-off 2.0¢ per share were paid on 23 May 2019 (US$29.4 million) and the 2019 interim dividend of 3.0¢ per share was paid on 18 October 2019 (US$11.0 million).

The Board has declared an interim dividend of 3.2¢ per share in accordance with 888’s dividend policy, plus an additional one-off 2.8¢ per share, bringing the total to 6.0 ¢ per share (H1 2019: 3.0¢ per share) payable on 4 November 2020.

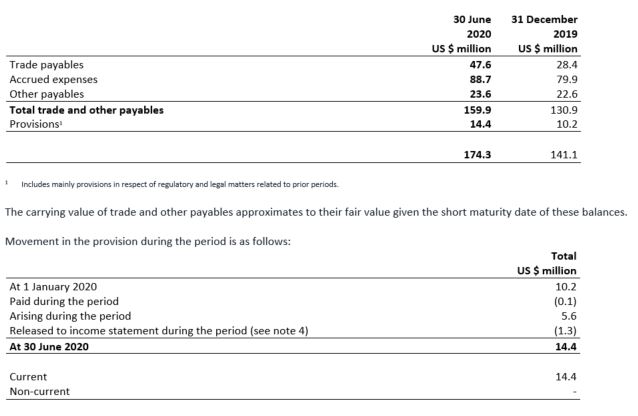

9 Trade, other payables and provisions

10 Interest-bearing loans and borrowings

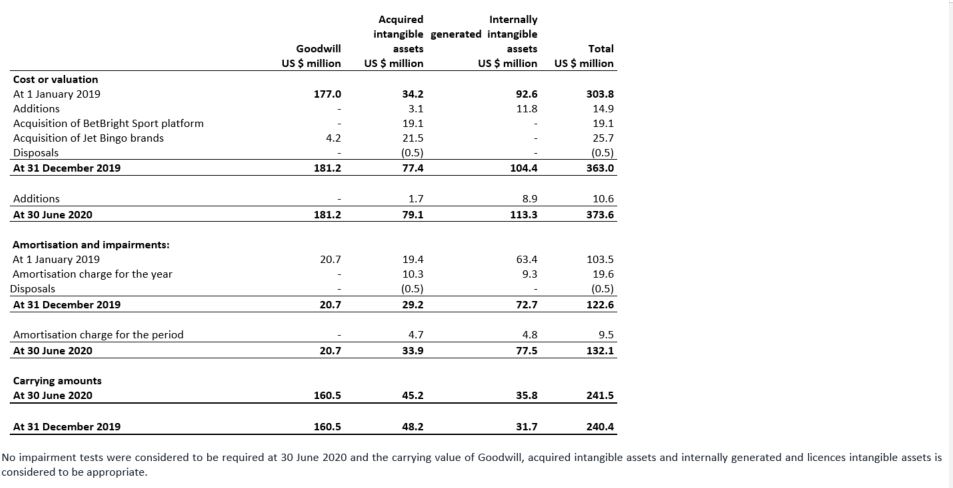

11 Goodwill and other intangible assets

12 Fair value measurements

At 30 June 2020 and 31 December 2019, the Group’s equity investment of US$0.2 million is measured at fair value (level 2). For the remaining financial assets and liabilities, the Group considers that the book value approximates to fair value.

There were no changes in valuation techniques or transfers between categories in the period.

Statement of Directors’ Responsibilities

The Directors confirm that to the best of their knowledge:

- The condensed set of financial statements, which has been prepared in accordance with IAS 34 “Interim Financial Reporting” as issued by the IASB and adopted by the EU, gives a true and fair view of the assets, liabilities, financial position and profit of the company and the undertakings included in the consolidation as a whole.

- The interim management report includes a fair review of the information required by:

- a) DTR 4.2.7R of the Disclosure and Transparency Rules, being an indication of important events that have occurred during the first six months of the financial year and their impact on the condensed set of financial statements; and a description of the principal risks and uncertainties for the remaining six months of the financial year; and

- b) DTR 4.2.8R of the Disclosure and Transparency Rules, being related party transactions that have taken place in the first six months of the current financial year and that have materially affected the financial position or performance of the entity during that period; and any changes in the related party transactions described in the 2019 Annual Report and Accounts.

The Directors of 888 Holdings plc are as listed in the 888 Holdings plc Annual Report and Accounts for 31 December 2019, with the addition of Limor Ganot, who has been appointed to the Board as an independent non-executive director with effect from 1 August 2020.

A list of the current Directors is maintained on the 888 Holdings plc website: corporate.888.com.

By order of the Board of 888 Holdings plc.

Independent Review Report to 888 Holdings plc

Introduction

We have been engaged by the Company to review the condensed set of financial statements in the half-yearly financial report for the six months ended 30 June 2020 which comprises the Condensed Consolidated Income Statement, the Condensed Consolidated Statement of Comprehensive Income, the Condensed Consolidated Balance Sheet, the Condensed Consolidated Statement of Changes in Equity, the Condensed Consolidated Statement Cash Flows, and the related notes to the financial statements 1 to 12. We have read the other information contained in the half yearly financial report and considered whether it contains any apparent misstatements or material inconsistencies with the information in the condensed set of financial statements.

This report is made solely to the company in accordance with guidance contained in International Standard on Review Engagements 2410 (UK and Ireland) “Review of Interim Financial Information Performed by the Independent Auditor of the Entity” issued by the Auditing Practices Board. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the company, for our work, for this report, or for the conclusions we have formed.

Directors’ Responsibilities

The half-yearly financial report is the responsibility of, and has been approved by, the directors. The directors are responsible for preparing the half-yearly financial report in accordance with the Disclosure Guidance and Transparency Rules of the United Kingdom’s Financial Conduct Authority.

As disclosed in note 1, the annual financial statements of the group are prepared in accordance with IFRSs as adopted by the European Union. The condensed set of financial statements included in this half-yearly financial report has been prepared in accordance with International Accounting Standard 34, “Interim Financial Reporting”, as adopted by the European Union.

Our Responsibility

Our responsibility is to express to the Company a conclusion on the condensed set of financial statements in the half-yearly financial report based on our review.

Scope of Review

We conducted our review in accordance with International Standard on Review Engagements (UK and Ireland) 2410, “Review of Interim Financial Information Performed by the Independent Auditor of the Entity” issued by the Auditing Practices Board for use in the United Kingdom. A review of interim financial information consists of making enquiries, primarily of persons responsible for financial and accounting matters, and applying analytical and other review procedures. A review is substantially less in scope than an audit conducted in accordance with International Standards on Auditing (UK) and consequently does not enable us to obtain assurance that we would become aware of all significant matters that might be identified in an audit. Accordingly, we do not express an audit opinion.

Conclusion

Based on our review, nothing has come to our attention that causes us to believe that the condensed set of financial statements in the half-yearly financial report for the six months ended 30 June 2020 is not prepared, in all material respects, in accordance with International Accounting Standard 34 as adopted by the European Union and the Disclosure Guidance and Transparency Rules of the United Kingdom’s Financial Conduct Authority.