Philippine President Rodrigo Duterte is quite an interesting enigma. He’s sort of like Donald Trump in personality and approach to exercising power. If Trump weren’t so constrained by the U.S. Constitution, he’d act more like Duterte. Trump has to search for technical loopholes that allow him absolute, or near absolute power, like using Cold War era legislation that allows a sitting President to almost unilaterally institute any tariff he wants on the grounds of national security. Duterte doesn’t have to find any such loopholes. He can just act. And he does.

Duterte has his passions and pet peeves, like his ruthless war on drugs (no comment), but he does seem to have a sense that decentralization and private ownership as opposed to government ownership is generally a good thing. Meaning, he’s no socialist ideologue with utopian views of equality, and he’s certainly no fan of political correctness. He does seem to have a basic understanding of how economies work in reality, unlike, say, Venezuela’s Nicholas Maduro or the late Hugo Chavez who are vastly more dangerous. Maduro or Chavez types will just keep pushing their catastrophic economic inanities until there is either absolutely nothing left and everybody starve to death (which is happening now in Venezuela), or they are assassinated (which almost happened earlier this month to Maduro).

Duterte has his passions and pet peeves, like his ruthless war on drugs (no comment), but he does seem to have a sense that decentralization and private ownership as opposed to government ownership is generally a good thing. Meaning, he’s no socialist ideologue with utopian views of equality, and he’s certainly no fan of political correctness. He does seem to have a basic understanding of how economies work in reality, unlike, say, Venezuela’s Nicholas Maduro or the late Hugo Chavez who are vastly more dangerous. Maduro or Chavez types will just keep pushing their catastrophic economic inanities until there is either absolutely nothing left and everybody starve to death (which is happening now in Venezuela), or they are assassinated (which almost happened earlier this month to Maduro).

Duterte may have a personal hatred for gambling, made clear in his recent suspension of any further licensing for casinos, but he knows where his money comes from and he’s not stupid enough to actively try to harm the gambling industry in his country. The suspension of new licenses will hurt consumers a little bit by raising prices due to constricting supply, but this is not the start of a crackdown on the gambling industry as a whole.

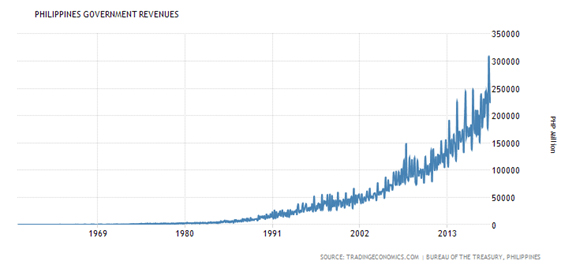

That the gambling industry is not coming under general attack is clear from the privatization of PAGCOR casinos this year. This move is likely to increase the efficiency of PAGCOR’s gigantic collection of gambling venues. The fact that Duterte, generally characterized as very controlling, is cool with this shows that he does have a good amount of sense. He seems to understand that allowing current casinos to operate independently will only help him collect more taxes, which is his real goal. Philippine tax revenues continue to roll in at records under Duterte, and he’s not going to endanger that.

The primary reason I believe that Duterte has come down so hard on illegal drugs is that drug dealers and users don’t pay taxes. Not that they have the option to do so, but if they had, he probably wouldn’t be advocating killing them.

Render to Duterte what is Duterte’s

There’s a simple lesson here regarding Duterte’s suspension of new gambling licenses: Do not mess with the man’s tax revenues. Render to Duterte what is Duterte’s. Otherwise he will lash out. His suspension of new licenses was prompted by what he perceived as a sweetheart deal for Hong Kong’s Landing International Development. The lease it signed with the government, at 70 years, was too long in his opinion, and the rent it signed for was too low. For sure there was back-scratching here, as there always is, but the bureaucrats at PAGCOR in charge of cementing this deal tried to take home a little too much bacon at Duterte’s expense, so he fired them all. He wants his share, and if he thinks some of his government henchmen are trying to cheat him out of it, he’ll go into punishment mode. Of course it doesn’t help that he hates gambling, which just made it easier for him to attack in this specific instance.

At bottom though, had the Landing deal given the government a larger cut on a shorter lease, this broad suspension may not have happened at all.

That said, Duterte is unlikely to cast his attack net any farther. Meanwhile, Landing still believes it has a valid lease and is continuing with its integrated resort project, but I doubt they’ll get very far. Defying Duterte in a country with a notoriously weak judiciary is probably not going to work.

The suspension is obviously bullish for casinos already in the country. Bloomberry and Melco should benefit over the long term, but it’s not an earth-shattering development that will move markets by itself. The Philippines’ gambling market is already pretty full. It primarily attracts tourists, and under Duterte’s watch, tourism from China specifically, where so much of the big gambling money comes from, is up 86% in 2016/17 compared to 2014/15. As long as the Philippines continues to attract more tourists, the gambling industry will continue to thrive, and Duterte will allow it to, hands off. In fact, if he really does hate gambling as much as he says he does, his antipathy may even serve as an added incentive to continue his hands-off policy with the industry. Maybe his personal feelings even had something to do with PAGCOR relinquishing control of its casinos to the private sector.

The emerging market tempest

Since the Philippines can be considered an emerging market economy, though technically it is grouped in the “Next Eleven,” what is happening with emerging market currencies now deserves a mention here. The collapse of the Turkish Lira has prompted routs in the emerging market currencies of Argentina, Brazil, South Africa and others. If the Philippine Peso gets caught up in this storm, then there could be some trouble short term. But it doesn’t look that way judging by the numbers.

A currency collapse cannot happen without grossly irresponsible inflationary monetary policy paving the way. Turkey’s money supply, for example, has octupled since 2006. Argentina’s has sexdecupled, or twice octupled. The Philippine Peso supply has less than quintupled, up 4.6x over the same time period, which isn’t the paragon of virtuous monetary policy, but it won’t subject the Peso to the savagery of what’s happening to in Argentina or Turkey. Plus, the Philippines is not inundated with dollar-denominated debt like Turkey, which also protects the currency against too hard of a fall on forex markets. While the Philippine Peso is down 32% against the USD since 2013, the long term chart is not inexorable and parabolic as it is with the Argentine and Turkish currencies, so it doesn’t look right now like the Philippines will get directly caught up in the emerging market domino effect.