Penn’s latest earnings just came in, and assuming the US economy continues apace and nothing major changes for the next 5 years or so in regional economies in the US, Penn looks to be in good shape. Revenues over $1.15B for an increase of $386M thanks to the Pinnacle acquisition, higher EBITDA, higher operating income, 2019 guidance of $163M in total earnings, and other numbers that sound great to investors’ ears.

Penn’s latest earnings just came in, and assuming the US economy continues apace and nothing major changes for the next 5 years or so in regional economies in the US, Penn looks to be in good shape. Revenues over $1.15B for an increase of $386M thanks to the Pinnacle acquisition, higher EBITDA, higher operating income, 2019 guidance of $163M in total earnings, and other numbers that sound great to investors’ ears.

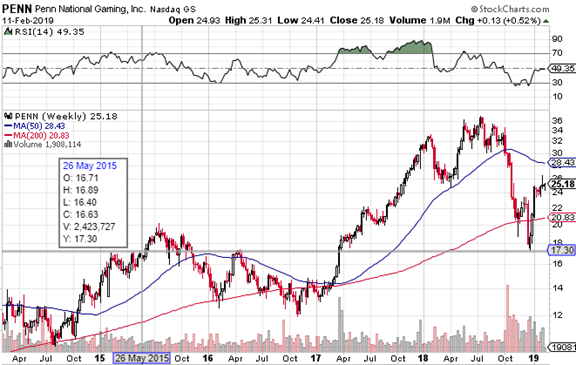

As long as everything stays stable, Penn remains in a good situation. However, a quick glance at the stock’s long term chart shows that it is anything but stable. Shareholders are riding on leveraged buyouts that for now are working out, but at the expense of heavy indebtedness that threatens long term losses should anything upset the apple cart. Consider, just the recent stock market plunge late last year, triggered without any serious economic earthquakes, brought shares down 53%, rivaling Penn’s decline during the 2008 financial crisis of about 70%.

The bullish argument is as follows. At the end of 2008, Penn had $2.725B in debt with a market cap of only $515M at the lows. Now it has total debt including triple net lease obligations of $4.5B and a market cap of $3B, so what’s the problem? If Penn shares survived 2008 and even thrived in its aftermath to new highs and enviable acquisitions, up until last August at least, then it certainly looks to be in a better situation now. A 53% fall and the regional casino operator has leverage of 150%, not so bad considering it now has Pinnacle under its belt, plus a new property at Greektown in Detroit, plus Margaritaville Resort Casino as of January 1st.

But there’s a big difference between ten years ago and now. Back then, Penn’s debt was variable and interest rates plummeted in the wake of 2008 as the Federal Reserve unleashed the most explosive money-printing operations in human history totaling over $10 trillion strewn around the world and into the banking system. Penn got through the financial crisis with more or less stable revenues, but higher operating expenses, which brought shares way down along with the general panic out of equities at the time, but its balance sheet was sustainable due to the collapse in borrowing costs that ensued.

Still, that Penn’s share price was more than cut in half over the course of 5 months last year could be considered a bullish sign for bottom pickers. Now it has even more assets and revenue power and shares are at a major discount. That could be the case, but exposing a portfolio to share price movement this volatile is asking for trouble. This was the most extreme collapse in the history of Penn stock in terms of the depth of the fall over such a short time span, and there really was no major crisis anywhere.

As you can see from the chart above, the decline was halted at the $17.30 level, exactly where long term support was established in early 2015 and April 2016. If those levels are tested again for whatever reason, the next support zone is all the way down at around $14, another 45% fall from current levels. Such a move would push leverage up to 270%. We could be there by August or September. That’s the way the monetary picture is shaping up this year so far.

I also find some of the remarks by CEO Tim Wilmott confusing. Here’s a quote from the earnings release that is a bit strange:

“Our Board of Directors approved a new $200 million share repurchase program that is in effect until December 31, 2020. The new authorization reflects our confidence in the Company’s growing free cash flow from operations and is consistent with our historical practice of providing management the flexibility to allocate capital to share repurchases, debt reduction, and/or accretive transactions.”

Why mention debt reduction if the money is being spent on share repurchases? In Penn’s investor presentation following its acquisition of Pinnacle last year, it listed debt reduction as a priority. But it’s been going on more buying sprees since acquiring Pinnacle totaling $415M, plus the $200M share repurchase program authorized through 2020, plus the ongoing development efforts of $120M at Hollywood Casino York and $111M spending plans for Hollywood Casino Morgantown.

That’s $846M that could have been used to substantially reduce debt but Penn chose not to. So when exactly does debt reduction become a priority? Just because it’s in an investor presentation and the CEO says the words “debt reduction” doesn’t mean it’s actually going to happen. Granted, right now Penn doesn’t absolutely have to reduce its debt load, but just like it’s better to sell when you can rather than when you have to, it’s better to shape up your balance sheet when you can rather than when you have to.

Buried in Penn’s risk statement is the fact that any default could result in all debt becoming immediately due, allowing foreclosure of assets by creditors. This is what just happened to PG&E out in California. Term loans for Penn’s acquisitions are due in 2023 and 2025, which will absolutely require refinancing. Let’s hope they can get it.

What about the near term? I don’t see much upside for Penn at this point, because considering all the acquisitions just made, shareholders are going to start getting impatient for results. There are going to have to be significant earnings beats for the next two to three years to get shares back to up to where they were. To the downside, the deadline for a trade deal between the US and China is at the end of the month and prospects don’t look good for avoiding a tariff hike on Chinese imports to 25%. At the end of a credit cycle, this kind of added tax to the US economy could disrupt the entire system severely, primarily retailers. Even though Penn is not a retailer in the sense of it being a supermarket, its business is on the retail level and the same people that shop at supermarkets are those that patronize casinos. Additional tariffs could bring Penn shares down to lows quickly.

Penn would only be a buy if those levels are tested around $17.30 and a we see a double bottom, but even then it would only be for a quick trade.